This morning the Oregon Office of Economic Analysis released the latest quarterly economic and revenue forecast. For the full document, slides and forecast data please see our main website. Below is the forecast’s Executive Summary.

This economic expansion just celebrated its sixth birthday. In true-to-form fashion, the party included decent-but-not-great job gains and steady-but-subdued GDP growth. As such there are few signs from the U.S. economy that the expansion is about to end anytime soon, even if growth has been lackluster overall following the financial crisis. However, all expansions do end and the economy is more likely closer to its next recession than not. This is especially true as storm clouds are gathering offshore in the form of a stronger U.S. dollar, weaker global growth and a significant and potentially worrisome slowdown in China.

The Oregon economy is at full-throttle growth. Jobs and income are increasing as fast, if not faster than during the mid-2000s. Given demographic trends, such rates of growth are considered full-throttle. As in past expansions, Oregon has regained its traditional growth advantage relative to other states. Much of this advantage can be attributed to the state’s industrial structure and strong in-migration flows. More important are the indications that Oregon is seeing a deeper labor market recovery. Wages for the average Oregon worker are increasing quicker than in the typical state, and above the rate of inflation.

While growth rates, and the trajectory of the economy have improved considerably, Oregon is not yet fully healed from the Great Recession. The largest economic concern today is the participation gap – the difference between the share of the population with a job or looking for work and what the rate would be when operating at full strength. The improving economy is and will pull workers back into the labor force, helping to support future economic growth at the same time.

Oregon’s General Fund revenue growth slowed at the end of fiscal year 2015, as collections of personal income taxes dried up during May and June. Income taxes withheld out of paychecks slowed sharply, and the tax filing season ended with very weak payments as well. As a result of the weakness, General Fund revenues fell short of the May 2015 forecast by $56 million, which reduces the ending balances that were set aside by budget writers in June. Oregon’s tax collections have since picked back up, growing rapidly to start off fiscal year 2016.

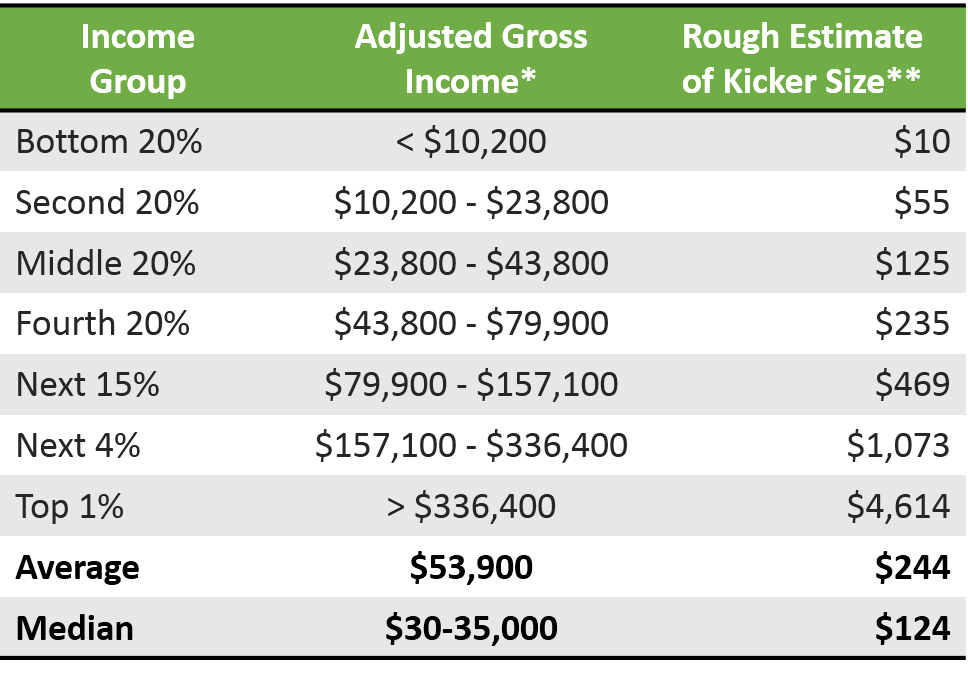

Although the General Fund ending balance for the 2013-15 biennium has become smaller, the associated reduction in available resources for the current biennium is largely offset by Oregon’s kicker law. With less personal income tax having been collected than was expected in May, revenues have moved closer to the kicker threshold, resulting in a smaller credit for tax filers next year.

Excluding corporate taxes, General Fund revenues exceeded the 2% kicker threshold by $111 million (0.7%), resulting in a kicker credit of $402 million. Due to actions taken by the 2011 Legislature, this kicker payment will take the form of a credit on 2015 tax returns rather than being issued as a check at the end of the year.

Looking ahead through the rest of the current biennium, the outlook for available General Fund and Lottery resources has remained relatively unchanged. Although downside risks are mounting, the underlying outlook for employment and income growth has remained stable, leading to a stable revenue outlook.

The revenue outlook is stable, yet uncertain. Volatility in equity markets is injecting a great deal of risk into the forecast. Oregon’s budget depends heavily on personal income tax collections tied to realizations of capital gains. These collections are extremely volatile, with revenues subject to the sometimes unpredictable behavior of investors. Although housing wealth has played a larger role in driving taxable capital gains over the last decade than in the past, earnings and losses in stock markets account for the lion’s share of movements in taxable capital gains in the typical year.

See our full website for all the forecast details. Our presentation slides for forecast release to the Legislature are below.

[…] assume job growth of 4,000 per month forever, without the economy overheating (which would tend to cause a recession) or without much stronger population […]

By: Jobs and Population Growth | Oregon Office of Economic Analysis on September 22, 2015

at 9:58 AM